Economic analysts and veteran bankers warned that the staggering volume of non-performing loans (NPLs) in 29 banks has moved beyond a financial hurdle into a systemic threat, effectively ‘choking’ the country’s liquidity and fueling inflationary pressures.

Nearly half of the scheduled banks, including 17 listed on the stock exchange, will be unable to pay dividends this year as the central bank enforces strict regulations to address the country’s high non-performing loan (NPL) crisis.

As per the Bangladesh Bank directive, any bank with a classified loan rate of 10 percent or higher is prohibited from distributing dividends, regardless of their net profit for the fiscal year. As of December 2025, 29 public and private banks reported double-digit default rates.

Selim Raihan, professor of DU and Executive Director of SANEM told UNB that the surge in defaulted loans is a symptom of long-term structural weakness.

"When nearly half of the banking sector sees double-digit defaults, it is no longer about individual business failures; it is about a culture of impunity. These 'frozen' assets are money belonging to ordinary depositors that is now trapped in the hands of a few, preventing the capital from being recycled into productive sectors,” he said.

Dr. Fahmida Khatun, Executive Director of the Centre for Policy Dialogue (CPD), emphasized the impact on the broader economy, such as- "The massive NPL volume is a major driver of our current inflation. Because banks cannot recover these funds, they are forced to increase the 'spread'—charging honest borrowers more to cover the losses of the defaulters. This raises the cost of doing business across the board,” She added.

According to the latest report of Bangladesh Bank, the default loans peaked at nearly 36 percent in September under the interim government's transparency measures, intensive recovery efforts and rescheduling brought the total down to Tk 5.57 lakh crore by the end of December. This represents 30.60 percent of the total outstanding loans in the banking sector.

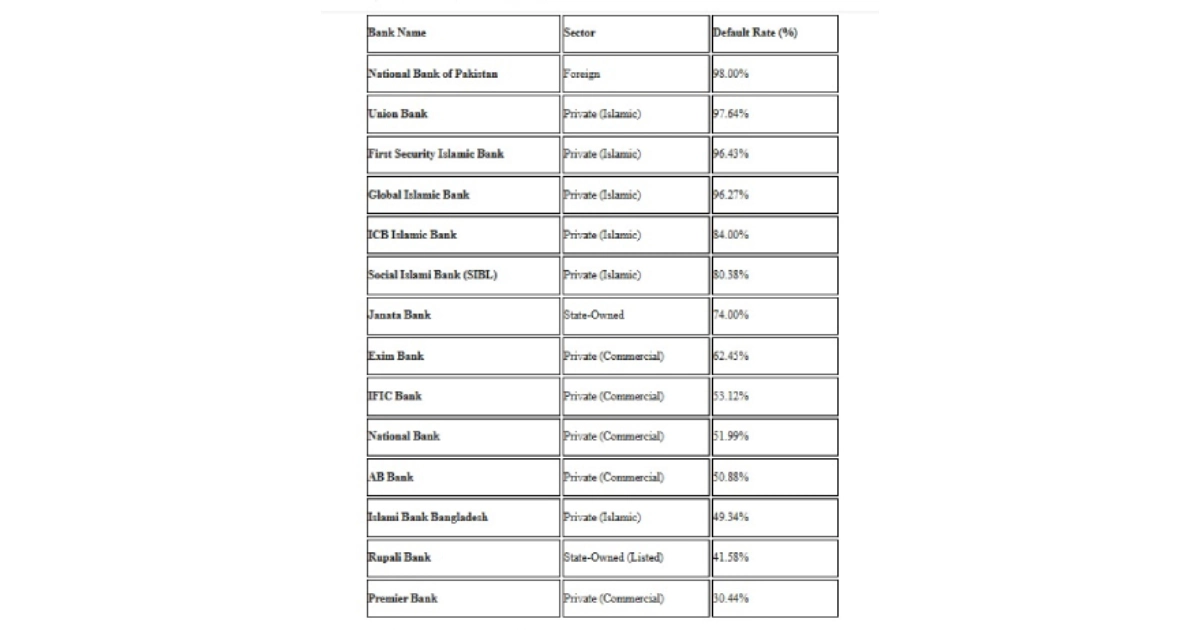

Among state-owned banks, Janata Bank holds the highest volume of defaults at Tk 72,152 crore, or 74 percent of its total loans. Rupali Bank, the only state-owned bank listed on the stock exchange, has a default rate of 41.58 percent or Tk 19,631 crore.

In the private sector, several banks—particularly those within the recently merged as Sammilito Islamic Bank—show alarming figures. Union Bank leads with a 97.64 percent default rate, followed closely by First Security Islamic Bank 96.43 percent and Global Islamic Bank 96.27 percent. Other major institutions, including National Bank 51.99 percent and Islami Bank Bangladesh 49.34 percent, also remain above the threshold.

A Managing Director of a leading private bank speaking on condition of anonymity, described a "liquidity trap" created by the NPL crisis.

He also said that some entrepreneurs are living luxurious lives and travelling abroad in business class air flights. But he is a bank loan defaulter. The total system is happening through a mechanism, where he avoids paying defaulted loans.

“Deposits come in, loans go out, and interest returns to fund new loans. When 30 percent of that cycle stops (due to defaults), the chain breaks. We are now in a position where we have to compete aggressively for deposits by offering high interest rates just to stay liquid. This high cost of funds makes it almost impossible to offer affordable credit to the RMG or SME sectors," he pointed out.

Summary of Major Defaulting Banks in Bangladesh (Based on December 2025 Data)